About the company: Company Name : Clean Science and Technology Ltd (CSTL) NSE Symbol : CLEAN CMP - Rs.1564 as on Sep 2, 2021.

Incorporated in 2003, Clean Science and Technology Ltd is one of the leading chemical manufacturers globally and as the name suggests its a eco-friendly manufacturer. It’s a family run business.

It manufactures functionally critical specialty chemicals such as :

Performance Chemicals - MEHQ, BHA, and AP

Pharmaceutical Intermediates - Guaiacol and DCC

FMCG Chemicals - 4-MAP and Anisole

Total - 7 products.

Company Market share in its products:

Source : RHP, Page-127

Sales and Distribution across the globe:

Page-135

Key Financials:

Page-129

Summary of Financials:

Pg-15

Product wise Revenue:

Performance chemicals – 70% of total revenues

Pharmaceutical Intermediates –17% of revenues

FMCG chemicals – 13% of revenues

Page-131

Clean Science Unique Manufacturing Process: (Vaporisation Technology - Low cost and High Margins)

First company in the world to manufacture Anisole through Vaporisation.

Source : SOIC

Conventional Manufacturing process by other companies:

Source : SOIC

Manufacturing Facilities:

Currently There are 2 facilities for the company.

Facility 1 → Kurkumbh, Pune, Maharashtra - 7 Units

Facility 2 → Kurkumbh, Pune, Maharashtra - 4 Units

All Facilities strategically located at Kurkumbh (Maharashtra) which is close proximity to the

JNPT port from where we export majority of our products.

Facility Wise product Manufacturing:

Pg-133

Additional Facilities under pipeline: (Location is same Industrial Area as mentioned above)

Facility 3 → which is proposed to be used to manufacture Anisole and certain Performance Chemicals, including MEHQ. We have recently commenced operations in one unit of Facility III.

Facility 4 → where we intend to manufacture stabilizer and other intermediates

for application in pharmaceutical, flavors and fragrance and agriculture industries.

Capacity Utilisation :

Pg-133

Various Products and its application:

Pg-126

Customers:

Our products are used as key starting level materials, as inhibitors, or as additives, by customers, for products sold in regulated markets. Key customers → Bayer AG, SRF Limited, Gennex Laboratories Limited, Nutriad International NV and Vinati Organics Limited

Products Overview:

Performance Products - 70% of Total Revenues

Monomethyl ether of hydroquinone (MEHQ)

Butylated Hydroxy Anisole (BHA)

Ascorbyl Palmitate (AP)

MEHQ:

MEHQ is an organic compound and a synthetic derivative of hydroquinone. Hydroquinone is basically an aromatic organic compound. CSTL is the only producer globally to manufacture MEHQ by the hydroxylation of anisole.

Uses : Monomers, Inks, API in the agrochemical and organic chemical manufacturing.

MEHQ is the intermediate of BHA and already company is forward integrated.

CSTL is World’s no.1 and its peers are Solvay and Camlin Fine science in No.2 and 3 globally.

Expected growth of this chemical for next 5 years globally: 5.8% CAGR

MEHQ is used as a stabilizer for acrylic acid and its salts. Global acrylic acid market exp to grow 6.6% CAGR and India Acrylic acid market exp to grow at 15.5% CAGR for the next 5 years.

Superabsorbent polymers (SAP) are commonly made from the polymerization of acrylic acid blended with sodium hydroxide - Uses : Infant diapers, feminine products and adult incontinence products

Estd 5 yrs growth of SAP globally - 5.4% CAGR

Current Demand of SAP is 100% in India and fully met by Imports and demand for SAP in India is expected to grow at about 11 - 12% between 2019 and 2025.

India Baby diapers and India Sanitary Napkin Market expected to grow 16.8% CAGR and 11.0% for the next 5 years.

BHA:

CSTL produce sulphur-free BHA when compared to its peers Solvay and Camlin Fine science.

USES: As an anti-oxidant in the food and feed industry, in animal feed and nutrition and personal care. Antioxidants are used for providing protection to essential nutrients such as vitamins, fats, and pigments from deterioration.

Indian animal feed market is poised to grow to ~$11B by 2025, growing at a CAGR of ~14%

Ascorbyl Palmitate - AP:

This chemical expected growth for next 5 years globally : 5.8% CAGR

Ascorbyl Palmitate (AP) is produced from ascorbic acid or vitamin C

Uses : Ingredient in anti-aging cosmetic products. Anti-aging products account for 17% of the total active personal care ingredients market (which is expected to grow further at a CAGR of 6.5% going forward).

Second largest producer in India

Pharmaceutical Intermediates –17% of revenues:

Guaiacol

Dicyclohexyl Carbodimide (DCC)

Guaiacol:

The global Guaiacol market is currently pegged at USD 309 million and is expected to grow at a CAGR of 1.3% from 2019 to 2025

CSTL is the third-largest producer globally and 2nd in India.

Solvay is the largest player in world

Camlin Fine Sciences is India’s the largest player

Uses : Precursor to manufacture APIs

Used in pharmaceutical industry for the production of cough syrups.

It is also used a key raw material for Vanillin, a food and flavour enhancer. Eg: Vanilla Ice-cream.

Guaiacol is used as a key starting material to produce APIs like Guaifenesin, Carvedilol, Ranolazine and Methocarbamol.

DCC:

CSTL began manufacturing DCC in 2020 and has become the largest DCC player in India and one of the largest players globally within just two years of commencing production.

CSTL manufactures sulphur-free DCC without using carbon disulphide. It acts as an anti-retroviral reagent and is primarily used in the pharmaceutical industry.

DCC is used as a key starting material for producing APIs like Valaciclovir, Amikacin and Glutathione, among others.

DCC is a powerful dehydrating agent commonly used for the preparation of amides, esters, and anhydrides. It is also used in peptide and nucleic synthesis. It is also used as a reagent in anti-retroviral drugs

Expected growth of this chemical for next 5 years globally : 4.9% CAGR

FMCG chemicals – 13% of revenues

4-Methoxy Acetophenone (4-MAP)

Anisole

4-MAP:

4-Methoxy-Acetophenone is an important spice, medicine, and makeup intermediate. 4-MAP is an aromatic chemical compound with an aroma described as sweet, fruity, nutty, and similar to vanilla. 4-MAP occasionally also has the aroma of butter or caramel.

The personal care industry in India is pegged at USD 14.3 billion, and expected to grow at a CAGR of 9.8% to reach USD 25 billion by 2025

Uses : As a cigarette additive, a fragrance, ingredient to manufacture UV Filter(most commonly used in sunscreens), and in food flavouring. It is also used as a chemical intermediate in manufacturing cosmetic additives like Avobenzone.

Expected growth for next 5 years globally : 3.6% CAGR Key Growth drivers for the next 5 years:

Anisole:

The global Anisole market was valued at USD 84.9 million in 2019 and expected to record a growth of 5.0% between 2019 and 2025. On a volume basis the demand of Anisole was around 34 KT growing at a CAGR of 4.5% – 4.8%.

Uses: Anisole is a precursor to perfumes, insect pheromones, and pharmaceuticals. Synthetic anethole is formulated from anisole. The compound is mainly made synthetically and is a precursor to other synthetic compounds.

Largest Manufacturer in world and accounting for 45% - 55% of the global capacity

Key positives:

Other companies seeing china as low cost competitor but CSTL exports 30-35% to China which proves they are the low cost producers in the world and only chemical company which exports to china.

Industry best EBITDA(55%), ROCE, ROE and margins.

Company is continuously focus and R&D with a robust R&D Team.

Company has strong relationship with customers and some customers have associated with the company for more than 10 years.

Largest producer of 4 out of 7 products globally.

Backward integrated especially the KSM(Key starting material) - Anisole is produced with vapor technology.

Key Risks:

Litigation against one of the Director - 2 criminal cases and Litigation against the company - 2 criminal cases and 1 Tax case (23.8 lacs)

Facility 4 Environment clearance will take time.

Addition of new products will affect the margins.

Exchange rate fluctuations may adversely affect our results of operations as our sales from exports and a significant portion of our expenditures are denominated in foreign currencies. Especially Phenol which is the largest contributor of Raw material cost.

Top 10 customers contribute 48% of revenues.

None of the company’s catalytic process are patented and competitors like Camlin Fine science can copy the process and capex expansion by Camlin will put margin pressure on CSTL.

Recent R&D Breakthrough on 27th August, 2021:

Continuing its pursuit of process innovation through catalytic technology, Clean

Science and Technology Limited (CSTL) is pleased to announce its foray into Hindered

Amine Light Stabilizers (HALS) series.

HALS series comprises a range of products which

find application in diverse end industries including polymerization inhibitor, water

treatment, paint industry, coatings industry etc. The estimated market size for HALS

series globally is approximately USD 1 billion. CSTL would be the first company to

develop HALS series in India.

Company has successfully developed key products in HALS series using in house R&D

capabilities, at lab and pilot scale.

The ongoing capex at Unit 3 is towards existing and new products. In Unit 3, Company

is launching first line of production dedicated towards HALS series, which is expected

to commercialize by H2 FY2023. Besides, additional production lines will also be

installed in Unit 4 for manufacturing products under HALS series.

Link - 79e5a335-7772-4156-9c99-cf4a582c0e45.pdf (959.0 KB)

Disc : Invested

Please feel free to add if I miss something.

Started in 1995 with clients such as Coca-Cola, Cellular One, Motorola, Ericsson which are facing operational challenges in India on account of limited availability of accurate maps. They obtained contracts to create digital maps that contained specific company information such as bottlers’ territories or topographic features such as high ground suitable for cell towers.

In 2004, company launched its digital map portal. Fast forward to today, company has mapped 10.5 M unique destinations, 6.4 M km of road, ~ 7500 cities at street level, 80 at address level, 3D, 2D landmarks in 86+ diff cities which is being updated Daily.

Product Offerings

1. Navigation Assistant Device

This is a navigation device embedded in dashboard of your 4W or 2W.

These are 3-5 years contracts with automotive makers.

Clients includes MG motors, Honda in 4W and Suzuki, TVS in 2W.

Company claims to have 80% market share in this segment.

They earn revenue per vehicle per year basis. Revenue will depend on no. of vehicle manufactured with MMI Navigation in a given year.

2. SaaS Products

(a) InTouch - IoT Platform & Telematics Platform

(Also, pitched as Digital Vehicle Twin)

This is cloud platform with various use cases majorly related to mobility like

Customizable Analytics Dashboard (Graphical representation of various parameter important to end user)

Live Tracking of Vehicle (includes drones), Vehicle level information - Speed, Location, Altitude , IoT GPS device status

Geo-fence Management : Geo-fencing is marking specific areas with geometrical figures (Polygon, Circle, etc) and tagging them as per business demand which will help in further location based analysis.

Company also provide bespoke solutions as per business requirements

~ 10k Downloads in Google Play store with 3.4 / 5 Rating.

Revenue Model - Subscription Based and as per Use Case

Vehicle Telematics : It includes GPS systems, onboard vehicle diagnostics, wireless telematics devices, and black box technologies to record and transmit vehicle data, such as speed, location, maintenance requirements and servicing, and cross-reference this data with the vehicle’s internal behavior.

(b) WorkMate

This Product intended to help companies with managing their field staff, location analysis for their clients, assigning tasks and generating reports related to same data

It’s also capable of working completely offline and gets automatically sync when back in internet connectivity

Display and branding is customizable to client

Clients includes PrintJet, Fullerton India, EMRI, Greenstarm SD Fine chem ltd.

~ 5k Downloads on Google Play store with 4/5 rating

Pay as you go model - revenue based on licenses per user per month.

(c) mGIS Tool

This is a visualization tool to perform analytics on geo-spatial data.

Some of the common metrics that could be tracked through this software like

Customer Location Visualization

Trade Area Analysis

Advanced Arithmetic Operations involving Elevations and Altitudes on 3D maps

Revenue Model - Subscription Based and as per Use Case

3. APIs / SDKs

API (Application Programmaing Interface) : In a nutshell, it is a piece of code that helps communication between two applications. So, if I need to insert a digital map or its related features in my personal app, I can use MapmyIndia API (Code) to get that data into my app and use it as per requirement.

SDK (Software Development Kit) : A kit or a package of tools, libraries, documentation, code samples, processes. Think of it as putting together a Squat Rack in your gym or that bed you bought from IKEA, you’ll need the base items, tools needed to put them together, assembly instructions and hence forth. An SDK might consists of several APIs and few other features around them.

All APIs / SDKs are subscription based freemium models and revenue depend on scale of client and number of transactions getting performed on application. There are several APIs / SDKs as below that company provides

Search APIs

Explore any address, location, place, Auto suggest, Nearby Places with Geo code or Reverse Geo code

Real time Map Updates, Auto Scalable, eLoc (a unique 6 char digital address of a particular house level location)

Apps includes McDonald’s, Yulu, PhonePe, Airtel

Routing and Navigation APIs / SDKs

Functions like Vehicle (Car, Bike, Truck, Pedestrian) Routing, Predictive ETA, Snap to Road, Turn-by-turn navigation, Drive range polygon (which will help in analysis of certain marked area)

Client includes MG, Mahindra, Amazon, HDFC, TVS, Suzuki

WorkMate APIs - APIs to get several data items from WorkMate App

mGIS APIs - Map and Location APIs, widgets, plugins and tools for developers to build advanced location-based applications - map visualizations in 2D/3D, Geo coding, search, routing, Geo-spatial analysis, AI-powered image analysis and more.

Global APIs - Map for 238 countries available

Personalization SDK

It helps build dynamic O2O (Online to offline) profiles for users or customers. This SDK help analyse profiles using algorithms to deliver personalized recommendations for products and services.

This also tracks buying patterns and create localised marketing campaigns

This has use cases in almost every major growing industry

4. IoT Products (Hardware Products)

IoT Products include GPS products to track vehicles, drone trackers, asset trackers. Other than that they also provide Drone cameras and various set of sensors

Map MyIndia’s Move App is used to track location, share location, Route summary and alert notifications

Some of the clients using their IoT products include Safe Express, TCS, AVIS

Industry Landscape and Competition

Regulation : Liberalization of Geo-spatial Sector

In Feb 2021, the Ministry of Science and Technology announced the deregulation of the Geo-spatial sector in India.

In the new Geo-spatial policy, there is no requirement to get approvals for the collection, preparation, storage and dissemination of Geo-spatial data and maps within India for Indian owned or controlled companies… It restricts foreign companies from doing granular level mapping - with a binding threshold of one meter in horizontal and three meter in vertical mapping making it difficult to create accurate maps for ADAS, HD, 3D, 360-degree street view, doing terrestrial survey and Indian territorial waters survey.

Since most of the foreign companies like TomTom and HERE use ADAS and HD tech for Navigation Maps, they’ll have to license the same through APIs from Indian Players.

Navigation Assistant Device and Mobility Related SaaS Products

Automobile Industry has been a major revenue contributor to map providers since last several years. This segment is consolidated among few players in particular region. MMI in India, TomTom and HERE Tech in UK and Map Box in US , has captured majority of the market.

This segment has been stagnant in last 2-3 years because of global automotive slowdown but is expected to pick back up in coming years as we are moving towards spectrum of autonomousity of vehicle, navigation system will become a integral part (both 4 and 2 wheeler).

After liberalization of Geo-spatial sector, we could see increased competition from other Indian Players getting aggressive in this space and we can also see some market share shift from foreign entities.

One of the recent news includes MG motors moved from TomTom to MMI in Aug 2021 in recently launched new models.

API / SDKs

As we discussed earlier, most of the application developers / companies prefer to include some functionalities of Location and Maps in their apps. APIs are highly preferred by companies to scale and grow their product quickly instead of re-inventing the whole wheel.

It is a fairly competitive space which leads API providers to spend on customer acquisitions through sales, getting interest of developers, free offerings upto a certain scale and at the same time, updating tech and investing in RnD.

Major competitors in this segment are Google Maps, TomTom, HERE Tech, Map Box, ESRI ArcGIS, Sales force Maps, Azure Maps, MapQuest

This segment is growing at a much faster pace, creating space for all competition to co-exist. With increasing penetration of internet and smartphones, growth will come from increasing use of location based apps, hence more transactions and increase in new applications using location based APIs.

The geo-spatial analytics space in India comprises of foreign players like ESRI, AutoDesk and Trimble. In addition to this, there are several other players like Rolta, RMSI, Infotech Enterprises.

Google : Elephant in the room

Spaces that google is present in this industry are as below :

Ad-sense - Google Maps earns majority of its revenue from Google’s Ad words and charges companies to advertise on google map app. For instance, if you search for Mumbai in Google Maps, it’ll show places, restaurants, cafe to visit.

APIs - Google Maps also provides APIs for different location based data and it’s pretty famous among developers however their prices are premium as comparison to other players and they also don’t provide HD, 3D Maps to doorstep level which might be a requirement for some e-commerce companies.

Navigation Assistant - Google stayed away from this segment until March 2017 when Google and Intel together with Volvo and Audi developed an Android Automotive Operating System (AAOS) combined with Google Automotive Services (GAS) which is a collection of applications and services like google maps, play, assistant, etc that OEMs can license and integrate into their in-vehicle infotainment systems. Volvo, Ford and GM are using AAOS with GAS.

In April 2019 Google opened up the APIs for developers to start developing applications for Android Automotive

Renault-Nissan-Mitsubishi alliance, one of the world’s top-selling automakers, has decided to go with Google’s Android operating system to run its dashboard information and entertainment features. A key reason cited previously by TomTom for Google’s contract wins was drivers’ desire to use a familiar, easy interface in their cars that is similar to the ones they are familiar with from their cell phones.

In September 2021, Honda announced that it would use Google’s Android Automotive OS in its cars starting in 2022.

Over the years, carmakers has been hesitant in giving full access of dashboard to Google due to data privacy concerns and willingness to own the branding for their dashboard. However, now with leading OEMs joining hands with google and well known superior quality product / brand of google, it will be the biggest risk for players in this segment like MMI, TomTom, HERE.

Financial Metrics

Overall Revenue Growth for company is flattish since 2018 but is expected to show high growth this year (31 % ▲ ) as per 1H22 Annualized numbers.

One of the reason for flattish performance is decline in IoT Products (GPS products) as they are mostly related to automotive industry which itself is facing strong headwinds from last few years and there is also a lot of local and foreign competition in hardware product market.

However, things get interesting when we look at segmental revenues below.

Another reason for overall revenue trend is Revenues from Automotive and Mobility (translates to Navigation Assistant, InTouch Platform and GPS products) has been declining rapidly majorly due to Slowdown in Automotive Industry. It has shown strong performance in 1H22 and expected to show high double digit growth in 2022.

Even with sharp decline in Automotive Segment, Consumer and Enterprise Segment (translates to APIs, SDKs, Customized Solutions and Analytics) is growing at rapid pace on account of exponential rise in digital economy over the globe.

Orderbook, which is projected on the basis of current orders + expected volume growth of clients for the next 3 Years and is subject to change in future based on Indutry demand, hence should be considered with pinch of salt. That being said, numbers provided for Orderbook are growing at exponential pace and should translate to high growth in Revenues, if all went well.

“70% of orderbook is based on projections of volumes from OEMs. The volume projections are based on either the projections shared by OEMs or based on the historical usage trends amongst certain other parameters. Our customers may terminate contracts before completion, negotiate adverse terms of the contract or choose not to renew contracts, which could materially adversely affect our business, financial condition and results of operations”

Margins

Variable cost in case of MMI are Software License Fee / Material Cost, Cloud Hosting Fee, Customer Customisation / Servicing.

Contribution margin has been increasing over the years mainly due to decline in Software License Fee and Customer Customization which generally relates to Automotive and Mobility Segment.

EBITDA Margins has also increased primarily because company has decreased non-permanent employees workforce and because of stable fixed cost and high contribution margin, EBITDA margins should be expected to increase in future with the rise in revenues.

Profit After Tax has also shown double digit growth because of increase in margins and one time exceptional ‘other income’ in 2021 after selling some investments / mutual funds.

Company has been surviving since two decades, on the basis of healthy cash flow generation. Due to asset light nature of business, EBITDA generally flows almost completely to Profits, CFO and Free Cash Flow. CFO in 2021 looks optically high because of changes in Financial Assets / Liabilities which will probably revert back to mean in coming years.

Growth Opportunities

Drone Industry

Drone industry is rising over the globe with the increased use cases and improved technology. Drone helps in quick field surveys, Supplying Essentials, Sensor Equipped for defense purposes, Geographic mapping, Safety Inspections,Crop monitoring, shipping and delivery.

Since GPS / GNSS (Global Navigation Satellite System) is a regulatory requirement for Drones, this could be a opportunity for MMI to strike deals at a nascent stage.

Rise in Electric Vehicles and Semi Autonomous Vehicles

As we move towards autonomous vehicle spectrum, Navigation Assistant will be required in most of the vehicles

Since, Automobile industry has seen increase in volumes, we can expect it to reflect in MMI Revenues

However, Google will remain a Challenge and need to have a keen eye how Google and other players are exploiting this market

Licensing of Maps

After the Geo-spatial liberalization in 2021, licensing of maps could appear as one of growth driver for MMI as Foreign Entities that provide HD and 3D Maps (TomTom and HERE Tech) will have to license map APIs from Indian Entities.

This could also benefit them bagging deals with potential clients

API revenue growth

Major Growth is surely expected from the APIs / SDKs which will be driven by

Increased traffic and transactions in existing clients like Paytm, PhonePe, Yulu

Addition of new clients which is expected with increased internet penetration, new start-ups and advancement of technology.

Vulnerabilities and Risks

Expansion of Google’s Android Automotive Operating System

Google is continuously finding ways to make Maps as its next billion dollar business. It was clear in 2018 when google did exponential price hike in APIs and then entered into Automotive segment .

Even though, currently main focus is in US and UK markets but it is a matter of time until google will try to capture the market in India.

Low RnD Spend

Considering its peers and being a tech company, RnD Spend is very low for MMI.

This could limit their scalability and could end up losing clients. They have also lost clients in previous years.

APIs/ SDK space is competitive.

API/ SDK segment, though highly profitable is competitive and price sensitive.

Switching Cost is moderate, Many companies have switched from using google map APIs to other providers after they’ve increased prices in 2018.

Increase of Supply

After new regulation, where Indian entities need no approvals for Map Data, new competition may arise from Indian players, hence challenging the economics of this industry

Customer Concentration

In the last three Financial Years, the number of customers that accounted for 80% of our revenue from operations were 17, 22 and 25 in Financial Years 2019, 2020 and 2021, respectively.

Though company is moving towards diversifying the revenue pool, losing key clients is a big risk to subscription revenues.

High Dependence on End User Industry

A large chunk of revenue comes from Automotive sector, hence revenues can get impacted in case of draw down in industry.

[Disclaimer: Holding a tracking position in this company. I’m not a registered Investment or Financial Advisor. Any information in this article is from personal research and is not intended as, and shall not be understood or construed as , financial advice. It’s very important to do your own analysis and reviewing the facts before making any investment based on your own personal circumstances. Kindly seek professional advice before taking investment decision.]

About the company: Company Name : Clean Science and Technology Ltd (CSTL) NSE Symbol : CLEAN CMP - Rs.1564 as on Sep 2, 2021.

Incorporated in 2003, Clean Science and Technology Ltd is one of the leading chemical manufacturers globally and as the name suggests its a eco-friendly manufacturer. It’s a family run business.

It manufactures functionally critical specialty chemicals such as :

Performance Chemicals - MEHQ, BHA, and AP

Pharmaceutical Intermediates - Guaiacol and DCC

FMCG Chemicals - 4-MAP and Anisole

Total - 7 products.

Company Market share in its products:

Source : RHP, Page-127

Sales and Distribution across the globe:

Page-135

Key Financials:

Page-129

Summary of Financials:

Pg-15

Product wise Revenue:

Performance chemicals – 70% of total revenues

Pharmaceutical Intermediates –17% of revenues

FMCG chemicals – 13% of revenues

Page-131

Clean Science Unique Manufacturing Process: (Vaporisation Technology - Low cost and High Margins)

First company in the world to manufacture Anisole through Vaporisation.

Source : SOIC

Conventional Manufacturing process by other companies:

Source : SOIC

Manufacturing Facilities:

Currently There are 2 facilities for the company.

Facility 1 → Kurkumbh, Pune, Maharashtra - 7 Units

Facility 2 → Kurkumbh, Pune, Maharashtra - 4 Units

All Facilities strategically located at Kurkumbh (Maharashtra) which is close proximity to the

JNPT port from where we export majority of our products.

Facility Wise product Manufacturing:

Pg-133

Additional Facilities under pipeline: (Location is same Industrial Area as mentioned above)

Facility 3 → which is proposed to be used to manufacture Anisole and certain Performance Chemicals, including MEHQ. We have recently commenced operations in one unit of Facility III.

Facility 4 → where we intend to manufacture stabilizer and other intermediates

for application in pharmaceutical, flavors and fragrance and agriculture industries.

Capacity Utilisation :

Pg-133

Various Products and its application:

Pg-126

Customers:

Our products are used as key starting level materials, as inhibitors, or as additives, by customers, for products sold in regulated markets. Key customers → Bayer AG, SRF Limited, Gennex Laboratories Limited, Nutriad International NV and Vinati Organics Limited

Products Overview:

Performance Products - 70% of Total Revenues

Monomethyl ether of hydroquinone (MEHQ)

Butylated Hydroxy Anisole (BHA)

Ascorbyl Palmitate (AP)

MEHQ:

MEHQ is an organic compound and a synthetic derivative of hydroquinone. Hydroquinone is basically an aromatic organic compound. CSTL is the only producer globally to manufacture MEHQ by the hydroxylation of anisole.

Uses : Monomers, Inks, API in the agrochemical and organic chemical manufacturing.

MEHQ is the intermediate of BHA and already company is forward integrated.

CSTL is World’s no.1 and its peers are Solvay and Camlin Fine science in No.2 and 3 globally.

Expected growth of this chemical for next 5 years globally: 5.8% CAGR

MEHQ is used as a stabilizer for acrylic acid and its salts. Global acrylic acid market exp to grow 6.6% CAGR and India Acrylic acid market exp to grow at 15.5% CAGR for the next 5 years.

Superabsorbent polymers (SAP) are commonly made from the polymerization of acrylic acid blended with sodium hydroxide - Uses : Infant diapers, feminine products and adult incontinence products

Estd 5 yrs growth of SAP globally - 5.4% CAGR

Current Demand of SAP is 100% in India and fully met by Imports and demand for SAP in India is expected to grow at about 11 - 12% between 2019 and 2025.

India Baby diapers and India Sanitary Napkin Market expected to grow 16.8% CAGR and 11.0% for the next 5 years.

BHA:

CSTL produce sulphur-free BHA when compared to its peers Solvay and Camlin Fine science.

USES: As an anti-oxidant in the food and feed industry, in animal feed and nutrition and personal care. Antioxidants are used for providing protection to essential nutrients such as vitamins, fats, and pigments from deterioration.

Indian animal feed market is poised to grow to ~$11B by 2025, growing at a CAGR of ~14%

Ascorbyl Palmitate - AP:

This chemical expected growth for next 5 years globally : 5.8% CAGR

Ascorbyl Palmitate (AP) is produced from ascorbic acid or vitamin C

Uses : Ingredient in anti-aging cosmetic products. Anti-aging products account for 17% of the total active personal care ingredients market (which is expected to grow further at a CAGR of 6.5% going forward).

Second largest producer in India

Pharmaceutical Intermediates –17% of revenues:

Guaiacol

Dicyclohexyl Carbodimide (DCC)

Guaiacol:

The global Guaiacol market is currently pegged at USD 309 million and is expected to grow at a CAGR of 1.3% from 2019 to 2025

CSTL is the third-largest producer globally and 2nd in India.

Solvay is the largest player in world

Camlin Fine Sciences is India’s the largest player

Uses : Precursor to manufacture APIs

Used in pharmaceutical industry for the production of cough syrups.

It is also used a key raw material for Vanillin, a food and flavour enhancer. Eg: Vanilla Ice-cream.

Guaiacol is used as a key starting material to produce APIs like Guaifenesin, Carvedilol, Ranolazine and Methocarbamol.

DCC:

CSTL began manufacturing DCC in 2020 and has become the largest DCC player in India and one of the largest players globally within just two years of commencing production.

CSTL manufactures sulphur-free DCC without using carbon disulphide. It acts as an anti-retroviral reagent and is primarily used in the pharmaceutical industry.

DCC is used as a key starting material for producing APIs like Valaciclovir, Amikacin and Glutathione, among others.

DCC is a powerful dehydrating agent commonly used for the preparation of amides, esters, and anhydrides. It is also used in peptide and nucleic synthesis. It is also used as a reagent in anti-retroviral drugs

Expected growth of this chemical for next 5 years globally : 4.9% CAGR

FMCG chemicals – 13% of revenues

4-Methoxy Acetophenone (4-MAP)

Anisole

4-MAP:

4-Methoxy-Acetophenone is an important spice, medicine, and makeup intermediate. 4-MAP is an aromatic chemical compound with an aroma described as sweet, fruity, nutty, and similar to vanilla. 4-MAP occasionally also has the aroma of butter or caramel.

The personal care industry in India is pegged at USD 14.3 billion, and expected to grow at a CAGR of 9.8% to reach USD 25 billion by 2025

Uses : As a cigarette additive, a fragrance, ingredient to manufacture UV Filter(most commonly used in sunscreens), and in food flavouring. It is also used as a chemical intermediate in manufacturing cosmetic additives like Avobenzone.

Expected growth for next 5 years globally : 3.6% CAGR Key Growth drivers for the next 5 years:

Anisole:

The global Anisole market was valued at USD 84.9 million in 2019 and expected to record a growth of 5.0% between 2019 and 2025. On a volume basis the demand of Anisole was around 34 KT growing at a CAGR of 4.5% – 4.8%.

Uses: Anisole is a precursor to perfumes, insect pheromones, and pharmaceuticals. Synthetic anethole is formulated from anisole. The compound is mainly made synthetically and is a precursor to other synthetic compounds.

Largest Manufacturer in world and accounting for 45% - 55% of the global capacity

Key positives:

Other companies seeing china as low cost competitor but CSTL exports 30-35% to China which proves they are the low cost producers in the world and only chemical company which exports to china.

Industry best EBITDA(55%), ROCE, ROE and margins.

Company is continuously focus and R&D with a robust R&D Team.

Company has strong relationship with customers and some customers have associated with the company for more than 10 years.

Largest producer of 4 out of 7 products globally.

Backward integrated especially the KSM(Key starting material) - Anisole is produced with vapor technology.

Key Risks:

Litigation against one of the Director - 2 criminal cases and Litigation against the company - 2 criminal cases and 1 Tax case (23.8 lacs)

Facility 4 Environment clearance will take time.

Addition of new products will affect the margins.

Exchange rate fluctuations may adversely affect our results of operations as our sales from exports and a significant portion of our expenditures are denominated in foreign currencies. Especially Phenol which is the largest contributor of Raw material cost.

Top 10 customers contribute 48% of revenues.

None of the company’s catalytic process are patented and competitors like Camlin Fine science can copy the process and capex expansion by Camlin will put margin pressure on CSTL.

Recent R&D Breakthrough on 27th August, 2021:

Continuing its pursuit of process innovation through catalytic technology, Clean

Science and Technology Limited (CSTL) is pleased to announce its foray into Hindered

Amine Light Stabilizers (HALS) series.

HALS series comprises a range of products which

find application in diverse end industries including polymerization inhibitor, water

treatment, paint industry, coatings industry etc. The estimated market size for HALS

series globally is approximately USD 1 billion. CSTL would be the first company to

develop HALS series in India.

Company has successfully developed key products in HALS series using in house R&D

capabilities, at lab and pilot scale.

The ongoing capex at Unit 3 is towards existing and new products. In Unit 3, Company

is launching first line of production dedicated towards HALS series, which is expected

to commercialize by H2 FY2023. Besides, additional production lines will also be

installed in Unit 4 for manufacturing products under HALS series.

Link - 79e5a335-7772-4156-9c99-cf4a582c0e45.pdf (959.0 KB)

Disc : Invested

Please feel free to add if I miss something.

With the proliferation of new users and consequent rise in flags (sometimes is subjective), here’s a small list to start with on what is actively discouraged at VP. This should aid both those who post and those flagging to keep VP a clean value-additive place for everyone.

So the keyword is non value-additive.

One or 2 liner or 1 para opinion posts/thank you posts/great job posts (once can always express through “Likes” or even message directly)

One or 2 liner or 1 para enquiry posts on topics that a simple google search will immediately point to

Targets/Price-Action posts - Why is it falling/Why is it going up/Opinions/Questions, and/or asking for reccos/entry price

(as different from industry/business-impacting data-points)

Name-calling and uncivil posts

Off-topic posts (including one off experiences with a product/service, detailed scuttlebutts at multiple stakeholders, though is encouraged)

Spam/Self-Promotional posts pointing to ones own blogs/twits/websites (everyone is encouraged though to share preferred details in their profile sections)

Newbie question posts (where someone has NOT bothered to read through earlier posts), asking same old questions that have been dealt with before, and the like

Excessive/Repetitive posts offering the same reasoning/arguments without taking the discussion forward

Direct uploads of non-public (not for free downloads) and/or proprietary (private) content

Copy/Paste of proprietary content (behind paywalls)

(small excerpts pointing to the main article may be okay, or if prior permission is obtained from author(s) for posting at VP)

This may seem like obvious Don’ts but not everyone is on the same page, especially newbies. Several folks have reached out to make this as transparent an exercise as possible, so here’s a first-cut from our first-hand experience over the last decade.

Moderation of a content-heavy forum like VP, is a huge task. And we cant thank enough the Moderators for doing what is essentially a thankless job. Moderators are human too, and errors can be made. We have acknowledged mistakes before. We iterate and learn along the way.

Thank you members for being alert and vigilant. Suggestions are welcome.

We will look to improve on this list again with your feedback and our active experience.

PS: Value-Additive posts are a no-brainer. We know it when we see it.

Something that takes the discussion forward. Data-points that connect the dots. Data-points that provide contrary facts to prevailing view/opinions, examples of our own workings, decision-making models, and the like. Something/anything that makes us better-informed on topic!

Our coverage of the midcap IT stories here at Valuepickr has missed Birlasoft, and I thought it’s time we keep a record of the investment thesis, and it’s development for posterity.

What’s the play?

Giant IT services companies like TCS and Infosys are the middlemen between customers that want to adopt modern solutions to cut costs, and pure tech companies such as Microsoft, Google, etc. that form their backbone.

We’ve seen the following trends in the last few years:

Having modern digital solutions to legacy problems are often an avenue to improve productivity and improve margins for companies. Covid has accelerated this spend, and will be a key driver of growth going forward.

Smaller IT companies have realised they can’t compete with giant incumbents and have healthy margins at the same time. The emerging solution seen across the pack is that they pick a few verticals and become the best solutions provider in their own niche.

Goal is to carve a niche in our verticals where we are better than the big players. We can’t solve every problem, but what we choose to solve, we can do much better than anyone else. - Dharmender Kapoor, interview with BQ, June 2021.

Okay, what are their verticals?

They have four main verticals. From the 2021 annual report:

Birlasoft helps customers in manufacturing to accelerate their Industry 4.0 adoption.

BFSI - to leverage open APIs and automate both front-office and back-office transformation;

Energy and Utilities - to enhance field collaboration and real-time service excellence, optimize operations and improve asset performance;

Life Sciences - to automate drug discovery and pharmacovigilance processes.

Here’s how the revenue mix has changed over the years:

Why now? What has the journey been in the last few years?

The story becomes interesting after 2015, when Birlasoft brought in Anjan Lahiri, and he worked on the company until 2019 when two things happened. They merged with KPIT Technologies and became the digital enterprise company of today, and Anjan Lahiri stepped down due to urgent personal reasons.

After this, they revamped the board, with Mr. Dharmender Kapoor taking over as MD, and in the last two years have onboarded senior talent. Their current CFO has been on the IBM senior management for 20 years, and this trend has continued if one looks at their hiring on Linkedin.

How has their business model evolved?

They’ve started focusing on their top clients and have trimmed tail accounts. Furthermore, they’ve started selling more to their top clients across their verticals. This is seen through three data points in FY21:

Lower $1 million deal wins, more $5 million deal wins.

97% of new deals are from existing clients.

Increasing TCV trend in deal wins, FY21 was their best year.

Annuity has improved from 60% in FY20 to 70% in FY21.

Deals are now multi service rather than single service. New deals don’t necessarily fall into one vertical.

They are constantly working on internal efficiency to improve operational metrics. The key metric management mentions repeatedly is the Days Sales Outstanding, and Utilisation rate:

Revenue per headcount across the quarters:

Q1FY22

Q4FY21

Q3FY21

Q2FY21

Q1FY21

Operating Profit (lakhs)

15100

15200

14400

11900

11300

Technical Employees

10445

9994

9416

8992

8865

Profit/Employee

1.44

1.52

1.52

1.32

1.27

This has been steadily improving, with a drop in the latest quarter. Management commentary on the same:

We lost $1 million of bottomline due to covid. Employees in India took leave when the second wave hit, and we didn’t dock their pay. Without this, the quarter would have been even stronger.

Accounting for this, the profit/employee for this quarter would be 1.52 as well.

The last data point is important while considering the difference in wage costs between India and the US.

From the latest earnings call on the onshore/offshore mix (paraphrased):

We usually hire locals (onshore) if there is a crunch, as the hiring lead time is a lot quicker than in India where there is a 3 month lead time. When we hire offshore, we replace onshore subcontractors. Clients are also on the same page with starting projects on site and finishing it offshore. We improve our margins, they get comfortable with deal structure.

Okay, numbers are improving. Do they have ambition?

Paraphrasing what Mr. Kapoor said in June’s interview with BloombergQuint:

By 2025, we want to have 7500 Cr. of revenues (3500 Cr. today, implies ~18% CAGR). We will do this by:

Growing top 30 accounts by > 20%;

Platform strategy: partnership with Azure / AWS to offer solutions across the value chain;

New channel for sales; good partnerships already in place.

Expecting profit CAGR to be much higher than revenue CAGR in the next 4 years. Profitability will grow. 3-4 quarters ago, this target of billion dollars was a dream. 2 quarters ago it became aspirational. Today, I’m far more optimistic and it’s looking like it can be a reality.

Absolutely no doubt that I and other top management will continue to work at Birlasoft until this goal is met. They’re motivated, excited, and handsomely incentivised to stay. We have our plans set in place for the next 3/4 years.

Financials and Cash Flows

Are currently debt free and have 1100 Cr. of cash in hand.

Risks

The vision is entirely dependent on Mr. Kapoor and his close circle. If they leave in the next few years, big questions to ask.

Dependent on their partnerships with SAP, Microsoft, AWS. Currently a Microsoft gold partner, which gives them benefits to companies searching for solutions providers.

Execution - Reliant on better deal wins and client mining to meet their 7500Cr. target.

When we acquired KPIT, used to think 75 million dollar deal wins were a great target for a quarter. Today, 200 million dollars should be the average every quarter.

However, Q1FY22’s deal wins have fallen short of their own metrics.

Their target of 1 billion dollars is a nice headline, but it implies a mid teen CAGR going forward. This is something we have heard from other midcap IT companies like FirstSource. Hence, is their target super normal?

Disclosure: Invested from lower levels, no recent transactions.

With current valuations, it’s becoming increasingly difficult to find low hanging value fruit. This post isn’t necessarily to offer a slam dunk investment opportunity, but to track a company here that may become more attractive/unattractive going forward.

Two amazing sources of information on the company:

BACKGROUND

A technical textile solutions company with humble beginnings manufacturing plastic products like HDPE/PP Fabrics & Woven Bags at Dholka (rural Ahmedabad) in 1985. Today the company employs 1700 employees and its yearly production is approx. 20,500 MTs of finished polymer based products.It’s mainly an exports company with very little domestic business.

MAIN PRODUCTS/SEGMENTS

The company is engaged in the business of technical textile, geotextile, and other allied products like manufacturing of PP/HDPE woven and non-woven fabrics and bags. Its products comprise PP Woven bags, fabric, box bag, ground cover, and lumber cover, mainly in the woven polypropylene market.

During FY2021 AGM, the management confirmed that it manufactures a building product for the US housing market in the form of Synthetic Roofing Underlayment.

If one carefully looks at the cover pages of the company’s past annual reports, for the first time in the FY2021 annual report, the management showed pictures of a house under construction with roofing underlayment and house wrap as their main products. In earlier years the company has always been showing silt fence, geotextile, and agri textile application pictures.

Below is the screenshot the latest AR cover page:

MAIN MARKETS/CUSTOMERS

SJPL is mainly an exporting company.

Almost 85% of the revenue contribution comes from the exports market.

The company doesn’t give any further breakdown of their sales.

As per our industry scuttlebutt, US is the biggest market for SJPL’s building product i.e. Synthetic Roofing Underlayment which it serves primarily through Epilay Inc and Edge Tech Partners LLC, and few much smaller players.

CURRENT MARKET/INDUSTRY TRENDS/SCUTTLEBUTT FINDINGS

Through scuttlebutt work we have confirmed that the roofing underlayment industry is going through a shift from Organic Felt (waterproofing tarp, saturated bitumen felt, asphalt felt) to Synthetic Underlayment. This migration started happening from about the 2011-12 period. Currently about 40% of the industry roofing contractors are still using the asphalt based traditional underlayment. And this shift is happening at a faster rate post COVID which is very positive for players like SJPL.

Two big problems with legacy underlayment products were 1) it was too heavy for roofers to carry to the roof 2) it was slippery as roofers laid the underlayment felt and walked on top of it to nail it down and prepare for adding the next layer on top of it. These are the two issues that were being addressed by the synthetic underlayment product for the roofing industry.

US Synthetic Underlayment market size is expected to be in the range of $1B to $1.5B. There are mainly two kinds of players in the Synthetic Underlayment roofing industry. 1) Branded full package (warranty) solution providers 2) Discretionary roofing solution providers who try to give the best solution at least possible cost, with or without warranty. Full package sellers are big branded players like GAF, Owen’s Corning, Dupont who give full warranty for all the layers of roof as a package. Generally there are 3-4 layers of roofing that goes into the making of a roof. Hence they command premium pricing. And most of them get their underlayment manufactured from India/China. Discretionary players sell only one layer in the form of synthetic underlayment.

Top 5 players command ~50% of the market and 45-50 players comprise the rest of the market. As mentioned before GAF, Owen’s Corning, Dupont are the biggest players dominating the market under full roofing package and full warranty business model.

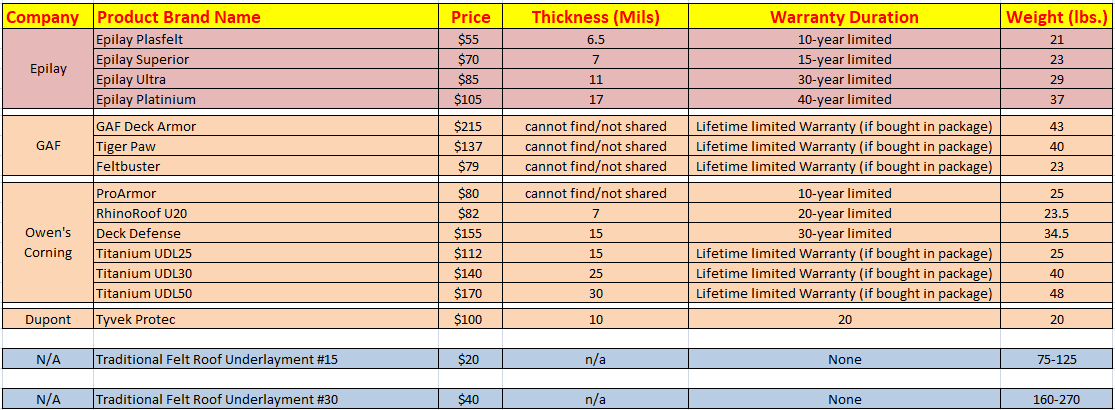

Below table gives product specification and pricing comparison of underlayment players:

Roofing contractors compare products mainly by price and thickness; more the thickness better the protection.

GAF, Owen’s Corning (OC) and Dupont are well established players serving the US roofing industry for decades. OC is a public company while GAF most probably is a private business. GAF’s main business model is to sell underlayments as part of a full roofing package with full warranty, hence premium pricing. GAF & OC’s lifetime warranty products are not directly comparable with Epilay’s products due to different business models but we can get an idea of how big the price difference is for similar underlayment with warranty being the main differentiation.

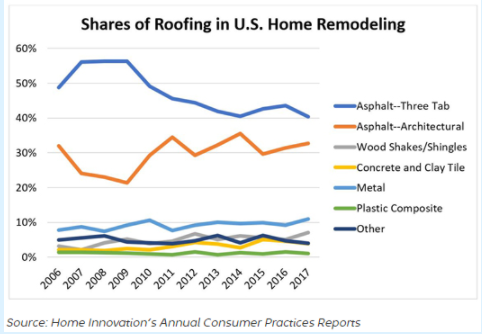

Asphalt shingles are used in more than 80 percent of home roofing and re-roofing projects in the United States. Regardless of the type of roof, underlayment will always be needed. But this is just to give an idea of roofing type breakdown.

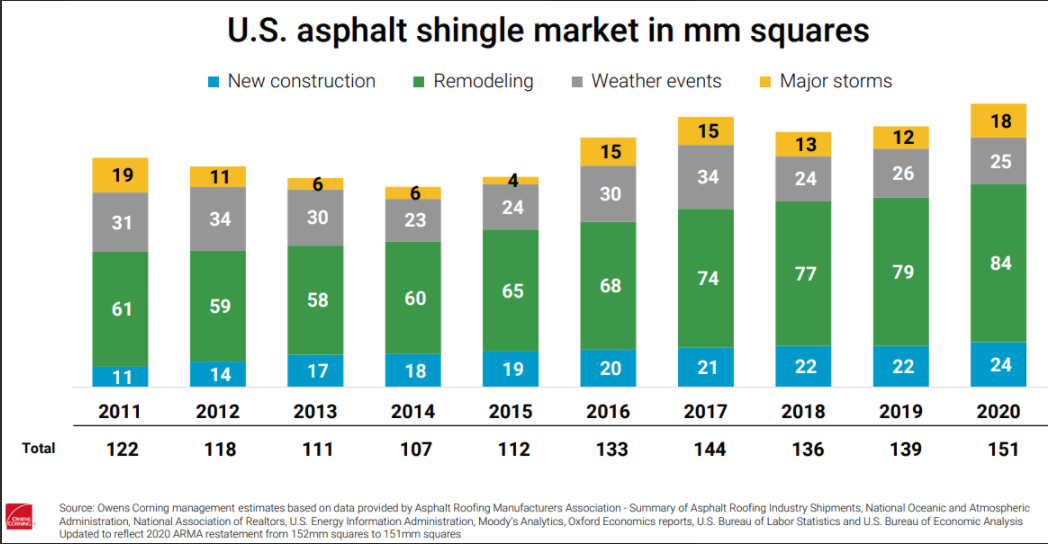

New construction demand annually has been around 15% of total asphalt shingle demand. Major portion of roofing demand comes from remodelling, weather events and storms. Most of the remodelling demand is likely non-cyclical. This slide indirectly confirms an industry expert’s assertion that the replacement market is the main market, and not new construction.

Miami-Dade County Data

The Miami-Dade County Product Control Approval System allows new and innovative ideas to be developed into practical, lasting and safe products. This approval process is recognized at both the national and international level. Product Control’s approval designation — Notice of Acceptance or NOA — has been recognized and accepted in Hawaii, Japan, South America, Guam and the Caribbean. The Product Control Approval System establishes a protocol to evaluate the standards of products used in construction in Miami Dade County. Miami-Dade County, with its inclusion in the High Velocity Hurricane Zone (HVHZ) has the most stringent code requirements of the Florida Building Code.

Roofing Underlayment sellers in the US need Miami Dade County NOA to be able to sell their products in the state of Florida and also in the US. There are about 36 sellers referenced in their website database who have their synthetic underlayment approved with Miami Dade County. Their products are manufactured mainly in China, India, and some in Canada.

Big companies like Dupont, Owen’s Corning, and others get their big brand underlayment products manufactured in India. Owen’s Corning in Silvassa and Dupont in Dadra. Ahmedabad/Dholka seems to be a big hub for the Polypropylene and Flexible Intermediate Bulk Container (FIBC) market. There seems to be other manufacturers in the Dholka area apart from SJPL like Veer Plastics Private Limited. [Scope for further scuttlebutt in India].

Roofing contractors are the final decision makers as to what underlayment goes into as part of the final installation of a roof depending on end customer warranty choices. Roofing contractors buy their underlayments from the distributors who ultimately stock up the products of various brands.

BULLISH VIEWPOINTS

FY2018 has been an important pivotal year for SJPL because it’s business performance has improved considerably since then. Prior to FY-2018 it’s EBITDA margin was in the range of 10%-12% which increased to 16%. Since then it’s EBITDA margins have increased above 20% for TTM ending September 2021. It’s sales have more than doubled in the last four years.

Current U.S. Housing Cycle has been going through a strong growth uptrend since 2010. About 500,000 homes were built in 2011 which has increased to about 1.3mn in 2020. Recovery since the 2008 crisis has been very smooth and consistent. Overall US construction spending has also followed a similar trajectory for both residential and non-residential segments.

US construction spending has been growing at about 4.8% CAGR in last 3 years. SJPL started selling Synthetic Roofing Underlayment from FY2018 and since then their sales are growing at about 13% CAGR. SJPL doesn’t share breakdown of their sales, however, we strongly believe that their Synthetic Underlayment segment sales is growing faster than the industry which is contributing to growth in market share.

Industry going through migration from asphalt based underlayment to synthetic underlayment. About 40% of the roofing contractors are still using asphalt based underlayment which is shifting to synthetic at a very fast rate, especially post covid.

While lot of players can and do manufacture roofing underlayment products competitively, selling in developed markets like US is tough, and totally dependent on local distribution strength/branding. Manufacturer - Distributor relationships seem deeply entrenched with very little incentive for distributors to switch vendors. SJPL’s biggest customer in the US, Epilay is growing at a fast rate and penetrating well in the US roofing market. It has a strong distribution network and sales team. It attends all major roofing exhibitions in the US, and carries out aggressive marketing campaigns and promotions for brand awareness.

Given roofing contractors are the final decision makers for what type of underlayment goes into the roofing installation - their main concern is to provide best quality at cheapest possible cost to end-customers who’s main interest is in the length of warranty they get for their roof. As seen from above pricing comparison table - Epilay provides warranty on all of its products at half the price, as compared to the full package solution brands. There’s incentive for more roofing contractors to shift towards offerings like Epilay’s which will in turn benefit SJPL.

SJPL has been a consistent performer from a business standpoint. Very impressive Sales & Profit growth over last 5 and 10 years.

Source: Screener.in

Management has guided for a 370-380Cr topline for FY2022 and decision on further CAPEX in FY22-23. SJPL did sales of 239 Cr in FY21.

Since bulk of the demand is replacement driven, new construction cycles have minimal impact on the overall demand.

Customer-driven value migration to higher-end building construction products is a distinct possibility

BEARISH VIEWPOINTS

SJPL’s current capacity may provide growth for next 1-2 years. Beyond that SJPL growth visibility is clouded as the management has not provided any timeline for new capacity expansion plans, as yet.

SJPL promoters have another unlisted entity Shakti Polyweave Pvt Ltd (SPPL) in a similar line of business with same product lines.

Unlisted entity has 1.5x the capacity as compared to the public entity. Future capex could possibly get diverted to private entity, at the expense of SJPL.

SJPL - 20,500 MTPA

SPPL - 32,000 MTPA

Typically low barriers to entry with high competition and no bargaining powers with the distributors and end customers. However, difficult to envisage main long-term customer Epilay, switching vendors.

There is very little product differentiation between the players in the industry. Everyone is making almost the same type of underlayment but packaged differently and wrapped with different warranties. It’s a commodity-plus business. However, the lowest cost producers/sellers can win market share which seems to be the case with SJPL and its customers in the last few years.

INTERESTING VIEWPOINTS

[TBD]

BARRIERS TO ENTRY

Barriers to entry for manufacturing the underlayment are low. Anyone with decent pockets can come in and set-up the manufacturing facility for synthetic underlayments. SJPL expanded its capacity from 12,000 MTPA to 20,500 MTPA in 2020-2021 at a cost of Rs. 46 Cr. SPPL recently expanded its capacity from 22,000 MTPA to 32,000 MTPA at a cost of Rs. 68.10 Cr.

Although someone with decent pockets can come in and set-up a manufacturing facility, but getting the right combination of a synthetic underlayment product and nailing down the final product can take upwards of 2-3 years. To quickly get the right product combination, it’s imperative to have people with deep polymer and polypropylene expertise.

Being able to manufacture required product isn’t enough to get one past the goalpost in developed markets. Barriers to selling the product in the US is very high. Having a recognised brand which has a wide distribution network in the US takes time, money, and consistent investment in market development. SJPL’s biggest customer in the US has got a strong brand and good sales & marketing team for pushing their products.

Synthetic underlayment products need to be approved at County and State level in many of the states of the US. Getting such approvals is a lengthy and cumbersome process as it can possibly take about 1-2 years.

BUSINESS MODEL

Business model of SJPL is very straightforward. To be the least cost producer of the synthetic underlayment and other products that it makes and enable its customers in the US to be least cost sellers for them to compete with the large brands who provide full roofing package solutions.

VALUATION MODEL

On a TTM basis, SJPL is available at ~14.5x PE given current market cap of Rs. 818 Cr.

If SJPL were to deliver a topline of 360-370cr for FY22 with current margins sustaining, it could possibly deliver a bottom line of around 65 Cr. This gives us a forward PE of 12.6x.

CORPORATE GOVERNANCE SCAN

Promoters having a private entity which runs a similar line of business is the biggest red flag for this story. Since SJPL has grown at a very consistent pace in the recent past, it gives some comfort that the management might continue to invest in both SJPL and unlisted SPPL, without prejudice to either.

Our coverage of the midcap IT stories here at Valuepickr has missed Birlasoft, and I thought it’s time we keep a record of the investment thesis, and it’s development for posterity.

What’s the play?

Giant IT services companies like TCS and Infosys are the middlemen between customers that want to adopt modern solutions to cut costs, and pure tech companies such as Microsoft, Google, etc. that form their backbone.

We’ve seen the following trends in the last few years:

Having modern digital solutions to legacy problems are often an avenue to improve productivity and improve margins for companies. Covid has accelerated this spend, and will be a key driver of growth going forward.

Smaller IT companies have realised they can’t compete with giant incumbents and have healthy margins at the same time. The emerging solution seen across the pack is that they pick a few verticals and become the best solutions provider in their own niche.

Goal is to carve a niche in our verticals where we are better than the big players. We can’t solve every problem, but what we choose to solve, we can do much better than anyone else. - Dharmender Kapoor, interview with BQ, June 2021.

Okay, what are their verticals?

They have four main verticals. From the 2021 annual report:

Birlasoft helps customers in manufacturing to accelerate their Industry 4.0 adoption.

BFSI - to leverage open APIs and automate both front-office and back-office transformation;

Energy and Utilities - to enhance field collaboration and real-time service excellence, optimize operations and improve asset performance;

Life Sciences - to automate drug discovery and pharmacovigilance processes.

Here’s how the revenue mix has changed over the years:

Why now? What has the journey been in the last few years?

The story becomes interesting after 2015, when Birlasoft brought in Anjan Lahiri, and he worked on the company until 2019 when two things happened. They merged with KPIT Technologies and became the digital enterprise company of today, and Anjan Lahiri stepped down due to urgent personal reasons.

After this, they revamped the board, with Mr. Dharmender Kapoor taking over as MD, and in the last two years have onboarded senior talent. Their current CFO has been on the IBM senior management for 20 years, and this trend has continued if one looks at their hiring on Linkedin.

How has their business model evolved?

They’ve started focusing on their top clients and have trimmed tail accounts. Furthermore, they’ve started selling more to their top clients across their verticals. This is seen through three data points in FY21:

Lower $1 million deal wins, more $5 million deal wins.

97% of new deals are from existing clients.

Increasing TCV trend in deal wins, FY21 was their best year.

Annuity has improved from 60% in FY20 to 70% in FY21.

Deals are now multi service rather than single service. New deals don’t necessarily fall into one vertical.

They are constantly working on internal efficiency to improve operational metrics. The key metric management mentions repeatedly is the Days Sales Outstanding, and Utilisation rate:

Revenue per headcount across the quarters:

Q1FY22

Q4FY21

Q3FY21

Q2FY21

Q1FY21

Operating Profit (lakhs)

15100

15200

14400

11900

11300

Technical Employees

10445

9994

9416

8992

8865

Profit/Employee

1.44

1.52

1.52

1.32

1.27

This has been steadily improving, with a drop in the latest quarter. Management commentary on the same:

We lost $1 million of bottomline due to covid. Employees in India took leave when the second wave hit, and we didn’t dock their pay. Without this, the quarter would have been even stronger.

Accounting for this, the profit/employee for this quarter would be 1.52 as well.

The last data point is important while considering the difference in wage costs between India and the US.

From the latest earnings call on the onshore/offshore mix (paraphrased):

We usually hire locals (onshore) if there is a crunch, as the hiring lead time is a lot quicker than in India where there is a 3 month lead time. When we hire offshore, we replace onshore subcontractors. Clients are also on the same page with starting projects on site and finishing it offshore. We improve our margins, they get comfortable with deal structure.

Okay, numbers are improving. Do they have ambition?

Paraphrasing what Mr. Kapoor said in June’s interview with BloombergQuint:

By 2025, we want to have 7500 Cr. of revenues (3500 Cr. today, implies ~18% CAGR). We will do this by:

Growing top 30 accounts by > 20%;

Platform strategy: partnership with Azure / AWS to offer solutions across the value chain;

New channel for sales; good partnerships already in place.

Expecting profit CAGR to be much higher than revenue CAGR in the next 4 years. Profitability will grow. 3-4 quarters ago, this target of billion dollars was a dream. 2 quarters ago it became aspirational. Today, I’m far more optimistic and it’s looking like it can be a reality.

Absolutely no doubt that I and other top management will continue to work at Birlasoft until this goal is met. They’re motivated, excited, and handsomely incentivised to stay. We have our plans set in place for the next 3/4 years.

Financials and Cash Flows

Are currently debt free and have 1100 Cr. of cash in hand.

Risks

The vision is entirely dependent on Mr. Kapoor and his close circle. If they leave in the next few years, big questions to ask.

Dependent on their partnerships with SAP, Microsoft, AWS. Currently a Microsoft gold partner, which gives them benefits to companies searching for solutions providers.

Execution - Reliant on better deal wins and client mining to meet their 7500Cr. target.

When we acquired KPIT, used to think 75 million dollar deal wins were a great target for a quarter. Today, 200 million dollars should be the average every quarter.

However, Q1FY22’s deal wins have fallen short of their own metrics.

Their target of 1 billion dollars is a nice headline, but it implies a mid teen CAGR going forward. This is something we have heard from other midcap IT companies like FirstSource. Hence, is their target super normal?

Disclosure: Invested from lower levels, no recent transactions.

With current valuations, it’s becoming increasingly difficult to find low hanging value fruit. This post isn’t necessarily to offer a slam dunk investment opportunity, but to track a company here that may become more attractive/unattractive going forward.

Two amazing sources of information on the company:

Respected Investors, My name is Raghav Agarwal and I am a final year management student. I have been reading a lot on this wonderful platform and am finally able to present everyone with my first thread on Punjab Chemicals and Crop Protection Limited. I am open to your wonderful suggestions and your subtle criticisms and I hope we can have a fruitful discussion of this excellent company on this extraordinary platform.

*Punjab Chemicals & Crop Protection Limited

Overview*

Punjab chemicals and crop protection limited (PCCPL) is an agrochemical manufacturing company based in Punjab. The company was founded in 1975 with a vision of being an integral part of the strategic supply chain both domestically and globally. It started its manufacturing facility by initially producing generic chemicals like oxalic acid. It now caters to agrochemicals, pharmaceuticals, intermediates and industrial and special chemicals and is now manufacturing various types of agrochemicals, for example, Metamitron Ethofumesate, Diflufenican, Lenacil and Cyanazine, with Metamitron and phosphorus acid being the major products.

The company owns two manufacturing units in Punjab and has leased one in Pune. The company also has a wholly-owned subsidiary in Belgium by the name of SD Agchem, which caters to the demands in the European market. Agrochemicals hold 80-85% of revenues which further breaks into 3 segments which are herbicides, contributing to 55%, fungicides contributing to 30% and insecticides contributing to 15% to the revenues. Out of these Agrochemicals, CRAMS contribute 60-65% to the revenues and this division is expected to grow 3-4x in the coming years. The pharmaceutical’s division provides Analytical reagents to pharma companies like divis labs and Laurus labs. The top five Analytical reagents contribute to 30-40 Cr.

Export- domestic sales breakup comprises 63% of the revenues generated from exports and 37% from the domestic market. The domestic market further breaks down into two parts

Agrochemicals amounting to 40% and Intermediates amounting to 60% to the domestic segment.

Location-Wise Revenue Breakup FY21

Manufacturing Units

Derabassi, Punjab

Pimpri, Pune

Lalru, Punjab

Size

24Acres

1.5 Acres

23.5 Acres

Capacity

29700MT

3347 MT

5778MT

Capacity Utilization

80%

95%

73%

Certifications

ISO:14001

FSSI

ISO:14001, ISO:9001

Divisions

Agrochemical manufacturing

Industrial Division

Agrochemical manufacturing

Revenue Contribution

60%

5-10%

30-35%

Fundamentals

The company generated consolidated revenue of 678 Cr in the FY20-21 with an EBITDA of 97Cr and an EBITDA margin of 14.3%. The net profit was aggregated to 49.1Cr with a PAT margin of 7.2%. Punjab chemicals have an excellent ROEof 40% and ROCE of 32%, which showcases the excellent returns of the company on their equity as well as their capital employed.

Q2FY21

Change%

Q2FY22

FY20

Change%

FY21

Revenue

164Cr

27%

209Cr

550

23%

678

EBITDA

23 Cr

34%

31Cr

42

131%

97

EBITDA Margin

13.8%

1%

14.8%

7.6%

6.7

14.3%

PAT

12%

6%

18%

11

345%

49

PAT Margin

7.2%

1.4%

8.6%

2%

5.2%

7.2%

Accounting Ratios

FY21

Debt/Equity

0.5

ROE

39.83%

ROCE

38%

EPS

Rs.40

P/E

30.02

Interest Converge Ratio

10.3

Current Ratio

1.19

Promoter Holding

Image derived from Company’s Annual Report FY20-21

PCCPL VS Market Indices

Image derived from Company’s Annual Report FY20-21

Industrial Outlooks:

· Anticipated growth of the industry can be from $32 bn to $49 bn between 2021-2025 and grow at a CAGR of 6.3%.

· A big opportunity is created in the agrochemicals and speciality chemicals market because of the gaps in the supply chain that have been created because of the china plus one policy. This encourages the domestic producers to gain momentum in the production cycle and gain market share. This can be a big opportunity for a company like PCCPL which has a reputation for its contract manufacturing and its customer relationships. India imports 50% of the agrochemicals and keeping these will further boost low-cost manufacturing and will make India an important part of the supply chain.

· The export around agrochemicals in India is growing at a CAGR of 12% while domestic production is growing at a CAGR of 4%.

· India’s average per hectare consumption of agrochemicals is 1/10th of USA & UK and 1/20Th of Japan and China, this suggests that India’s demand for agrochemicals can still grow multifold and create robust demand for agrochemicals in the coming years. Food production is likely to increase in the coming years to cater the demands of the on a growing population. World food production is likely to increase by 70% by 2050.

· More than 100 agrochemical patents are getting expired by 2023. This will open up opportunities for CRAMS players and contract manufacturers and generic players including Punjab chemicals to manufacture new products for the excellent existing clientage as well as new players.

Key Growth and Profitability Drivers

The company aims to achieve a revenue of 1500 Cr within the next 3 years with the help of the following factors strengthening their objectives:

· Revenue Visibility: Punjab chemicals generated an order book of more than 1500 Crores for the FY21 with a stable EBITDA Margin of 12-14%. Improvement in the margins can be driven by better procurement, better efficiencies and cost savings and the company expects EBITDA margins to grow to 18-20% in the coming years.

· The management expects 2-3x growth in revenues from top customers which are UPL and ADAMA and which account for around 60% to revenues (35% and 25% respectively)

· Nippon Kayaku: The product that is being supplied to Nippon kayaku currently generates 10-12 Cr PA, with capacity utilisation of 80% for this particular product, The company believes that this product has the potential to generate 60-70 Cr to the revenue within12-18 months.

· Contracts with Singaporean MNC- The product that the company is manufacturing for the Singaporean company generates 12-15Crs to the revenue. The company aims to double that number in 2-3 years.

· The domestic formulation business is expected to grow 3-4 years, it currently contributes up to 50Cr to the top-line.

· Punjab chemicals is looking to increase revenues from its Industrial division because of the rise in demand for Phosphoric acid in pharmaceuticals as well as food and beverages. The company is already in talks with Coco cola to export phosphoric acid to their Korean and Singaporean factories. PCCPL already caters to the domestic needs of these companies and this segment adds around 50Cr to the topline. The management aims to double the segment revenue by next year.

Capex & Debt

· The company has planned a CAPEX of 150 Cr over the next 2-3 years and is planning to do a brownfield CAPEX at Lalru land where 6 acres are unutilized and available. The Asset turns from CAPEX of 150Cr will give out 3-4x returns and the total asset block will generate 200-300 Cr in the next 2-3 years.

· Company is planning to expand its Pune facility by planning to acquire the adjoining plot, because of the rise in demand for industrial chemicals like phosphoric acid that the company is producing for MNC’s like Coca-Cola and Pepsi Co.

· The company has a debt of around 80Cr and have managed to reduce it by 13cr in the last year. The management aims to go debt free in 2 years.

Risks and Concerns & Key Monitorables

· Change in Government and Government policies: Government policies related to agriculture and any alterations in agro expenditure and incentives can directly affect the company’s order book.

· Adverse climate and weather conditions: weather conditions like rainfall and pests directly affects the revenues of the company.

· Exchange rate Fluctuations, Registration period, supply security and quality from domestic supply.

· Promoter holding is low and has decreased since the last year by 2.02% from 40.03% to 39.22%.

· Registration processes for new products and molecules take time for registration and formulation.

· 60% of the revenues are generated through the two MNC’s UPL (35%) and ADAMA which contributes 25% to the top line, having concentrated revenue generation can cause concern if any issues regarding these companies take place.

· Raw Material- Raw material contributes 60% of the expenses and vary time to time. Any changes in Raw material costing directly affects the topline as well as the bottom line of the company.

Company’s Plus points

· Excellent Clientage and Long-term contracts: Punjab Chemicals have excellent customer relations with excellent clientage which includes UPL, ADAMA, Corteva, Coco cola, Pepsi Co, Divi lab, Laurus labs, to name a few.

· PCCPL contract manufactures niche products for clients which include Nippon Soda, Nippon kayaku, Corteva, Syngeta, Bayer etc and also manufactures intermediates for Zydus, Cadila, Laurus labs, Divi labs etc.

Opportunity In The CRAMS Segment

Crams segment contributes 60% to the revenues by agrochemicals and its successful execution remains the key re-rating trigger for growth. The company has the advantage of being a go-to CRAMS player for both domestic and international companies by gaining market share as the industry expands. PCCPL is expected to use this as an opportunity to grow with the help of:

(a) concrete relationships with global agrochemical companies.

(b) expertise in the business led by an experienced management team

(c) integrating R&D team of both companies (PCCPL and the partner

company) to provide better products.

(d) renewed relationships with domestic formulators with a strong base in the domestic market;

(e) strong order book of INR15bn as of FY’21 (revenue visibility for the next 2-3 years).

The Company continues to focus on new and promising products either for CRAMS or for direct sales to improve its revenue and profitability. While they have been able to get new clients in the CRAMS business with lucrative long-term agreements signed with few MNC’s.

MY VIEWS

• The company can double its EPS from Rs 40 in FY21 to anywhere between Rs80-100 in FY22-23.

• The company can achieve a short-term target of achieving Rs 850-1000Cr Revenues in the FY22 and can double its PAT from 49.1 Cr to 100 Cr by the end of FY23.