@ankitgupta wrote:

About the company

The Anup Engineering Limited (Anup) was incorporated in 1962 and is part of the Arvind group of Ahmedabad. The company was demerged from Arvind Ltd and listed as a separate entity in March, 2019. The company is engaged in the business of design and fabrication of process equipment which mainly includes heat exchangers, pressure vessels, centrifuges, columns/towers and small reactors that find applications in refineries, petrochemicals, chemicals, pharmaceuticals, fertilizers and other allied industries. Heat exchangers contributed 80 – 90% of the sales while remaining was contributed through sales of pressure vessels, centrifuges, columns/towers and small reactors.About the product

Heat exchangers are used to transfer heat or cooling from one liquid to another. Key industries served – oil & gas refineries, petrochemicals, fertilizers, chemicals, pharmaceuticals, food and other allied industries. The company has technical collaboration with Lummus Technology for special High Efficiency Heat Exchangers (Helixchanger).

(source: Anup Presentation)About the industry

Heat exchanger is a USD 21 billion industry globally – used to increase efficiencies. Largest players in the industry include: - Alfa Laval (>30% market share), Kelvion (Germany), Hisaka (Japan), SPX Flow/APV (US), SWEP (US). High profitability margins with many companies reporting gross margins of more than 45%. Alfa Laval has EBITDA margins of 14 – 15% while its Indian subsidiary also has EBITDA margins of 19%.

This is something which Credit Suisse prepared forx capital goods industry (was made for Alfa Laval):

Transformation Journey of the company

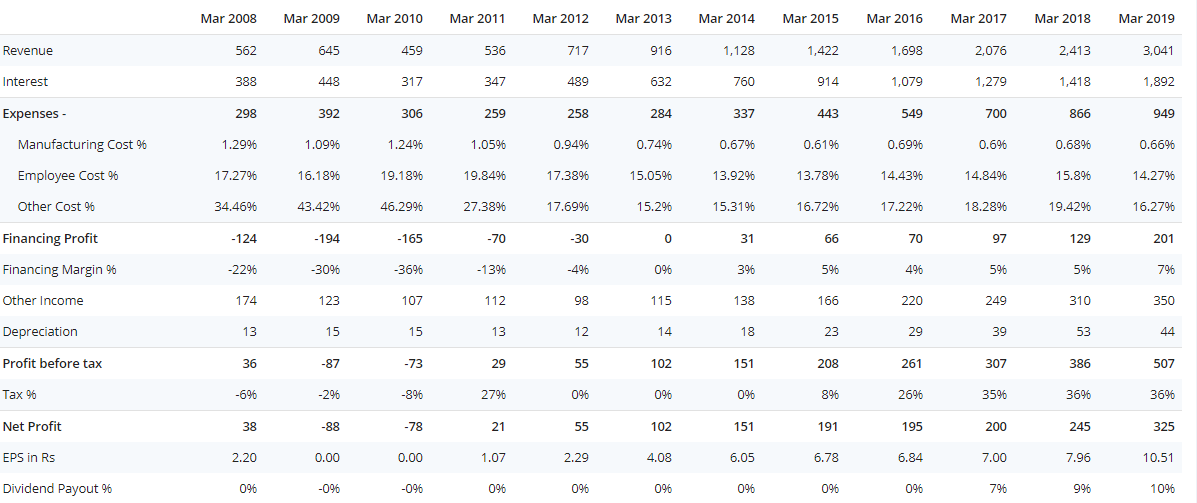

Despite being in the engineering segment since 1962, the company was not able to scale the business. However, the transformation of the company started when its current CEO – Mr. Rishi Roop Kapoor joined the company in 2010. Mr. Kapoor has pretty good reputation in the engineering industry and is an IIT Roorkee pass out. Prior to joining Anup, he was associated with Godrej and Boyce for more than a decade. The company has become a net cash company during the past few years and generates healthy cash flows.

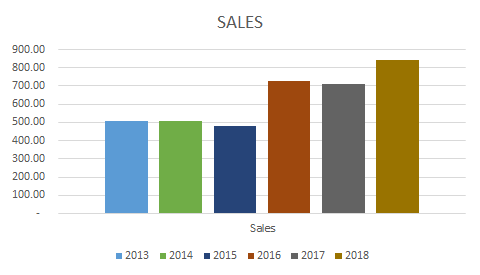

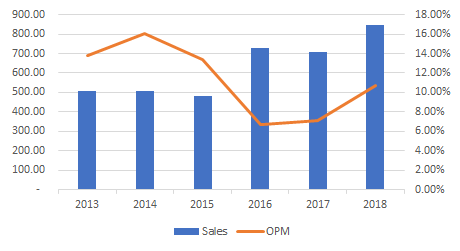

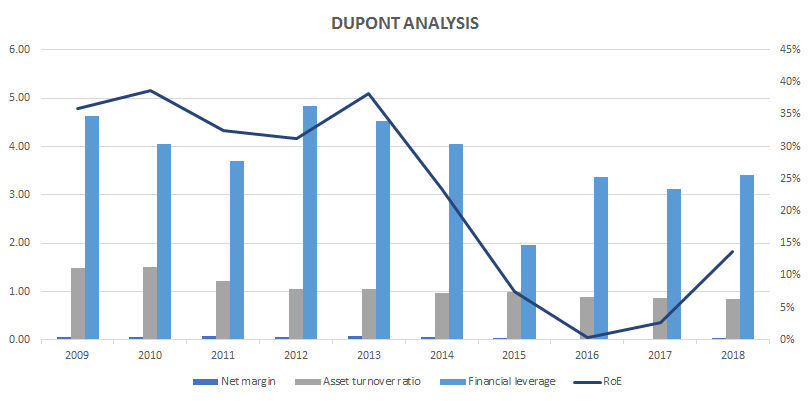

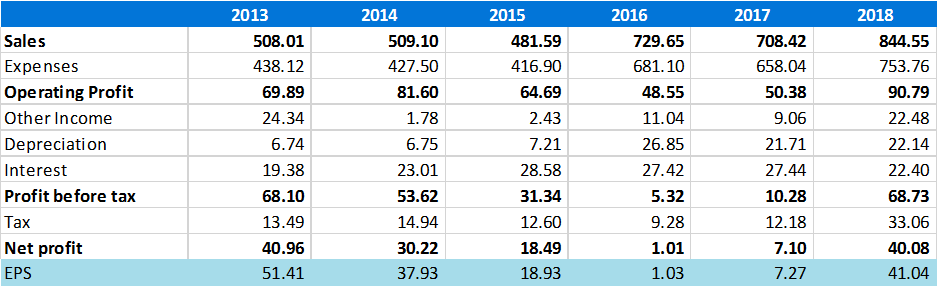

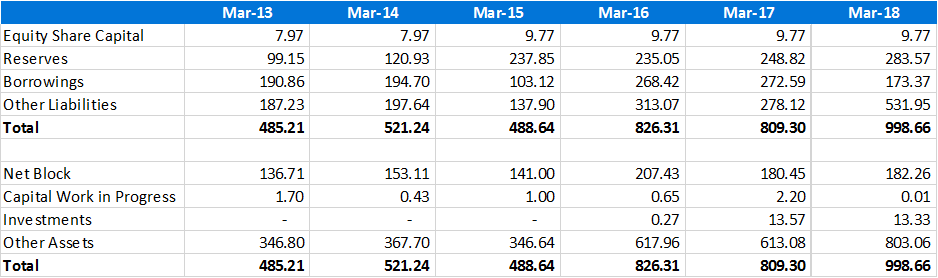

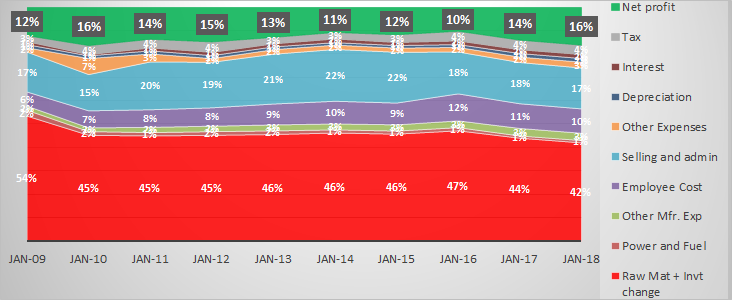

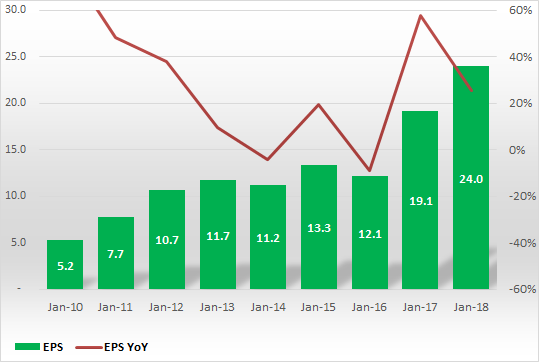

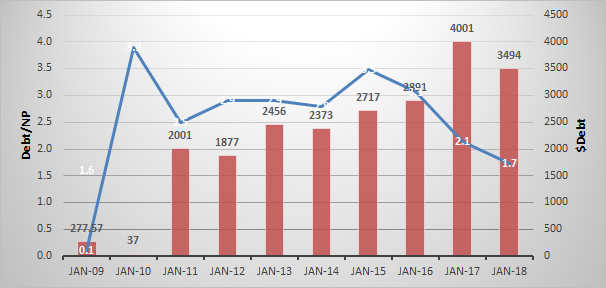

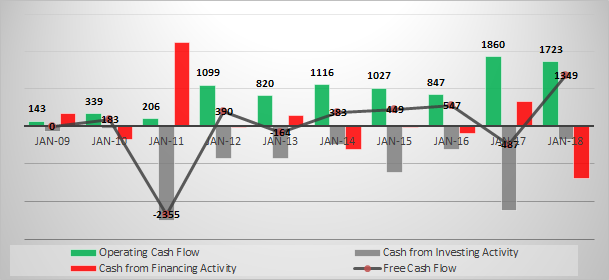

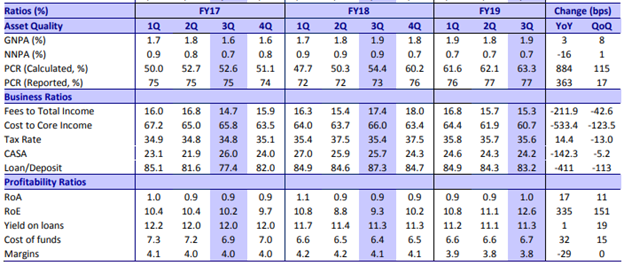

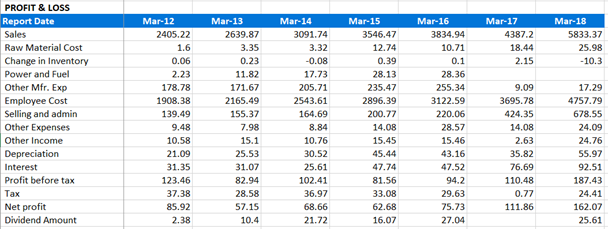

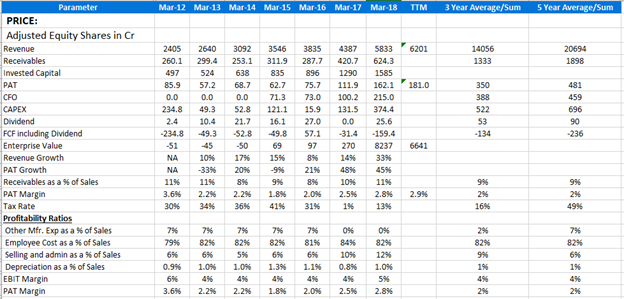

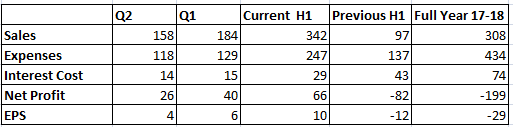

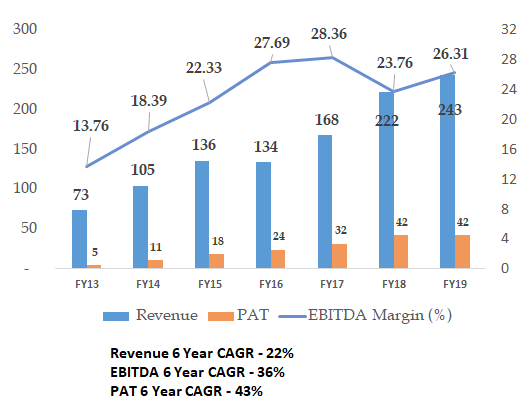

Key financials of the company:

Some of the measures taken to turn around the company include:

Increasing market reach with increasing exports: Over the years, the company has increased focus on export markets to reduce cyclicality associated with domestic markets.

Empanelment with large EPC players: Despite its relatively smaller size, the company has been able to empanel itself with large global MNC EPC players and customers including Lurgi, Linde, Jacobs, Mitsubishi etc. The company has executed large projects for companies including Dangote Refinery (one of the largest refineries in the world), Reliance, OMCs etc. The key client lists include:

(source: Company presentation)Improving designing and manufacturing capabilities – one of the rare companies with entire range of metal processing capabilities under one roof and excellent design capabilities

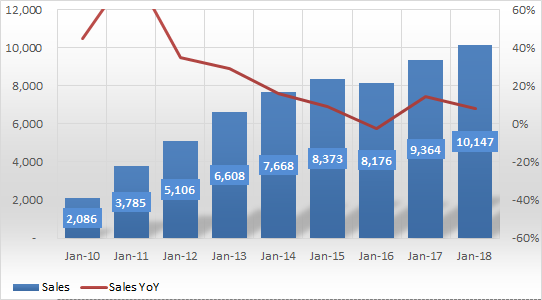

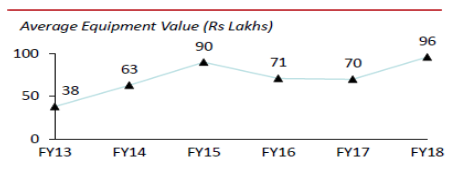

Increasing complexity and weight of the product manufactured: Over the years, the company has increased realization of the equipment manufactured by it as indicated in the graph below:

Sticking to deadlines and avoided paying liquidated damages - Gained confidence of customers leading to repeat buys - Liquidated damages are one of the biggest cost.

Competition

The company competes with pure play heat exchanger companies including Patel Airtemp and Tema India (unlisted company) as well as large capital goods companies inlcuding ISGEC and L&T. Have done a comparison on the margin profile of Tema and Patel with Anup. Companies like ISGEC and L&T have much diversified product profile and are not strictly comparable.

Anup has highest margins amongst its peers and even better than much larger and diversified player – One interesting thing to note is the healthy GM of pure play heat exchanger cos which is much more than many capital goods companies.

Way Forward

- All time high order book of the company – 300 crore by end of FY19 – largely from domestic market (might impact margins as guided by the management in its maiden concall post Q4FY19 results)

- Expanding capacities – Target to spend 150 crore in capex for brownfield capacity in Odhav, Ahmedabad and greenfield capacity at Kheda – 40 kms from Ahmedabad – to be funded through internal accruals

- Looking for further technological tie ups to enhance capabilities

- Targeting 1000 crore over then next 4 – 5 years

What is attractive about the company?

- Large industry size globally – new orders expected from all round the globe to improve efficiencies and cleaner fuels from refineries – Euro VI and BS VI implementation. Furthermore, the government owned OMC’s refinery are operating at 105 - 110% capacity utilisation and given the domestic demand of petrol/diesel with growth rates of 10 - 14% every year, these companies are looking at big capex over the next few years to expand their capacities.

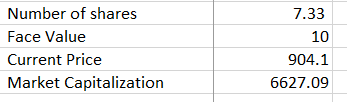

- Valuation – 42 crore PAT reported in FY19 and market capitalisation of around 500 crore currently. Healthy growth expected in revenues and PAT in FY20.

- Attractive industry dynamics with many players reporting attractive gross margins

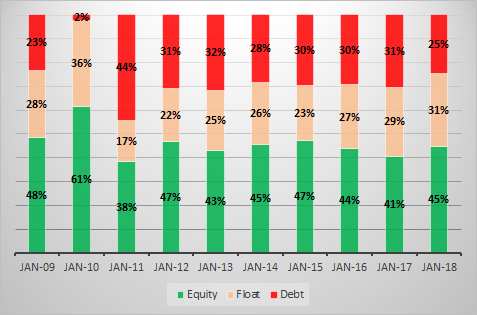

- Net cash balance sheet and healthy cash flows.

- Good feedback received from the industry peers about the company and top management.

Key Risks

- Lumpy business – less visibility of revenue beyond one year. Furthermore, revenue can remain volatile on quarterly basis based on dispatches and orders in hand.

- Largely dependent on oil & gas & petrochemical segment

- Peak margins given it reported EBITDA margins of 25% plus during FY19. However, some comfort can be derived from company’s track record of reporting margins in the range of 24 – 28% over the past 5 years.

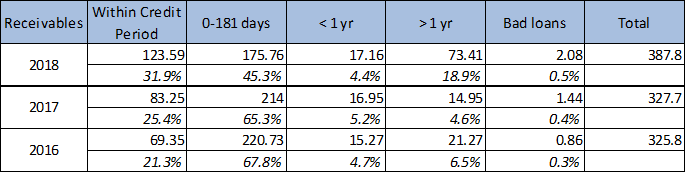

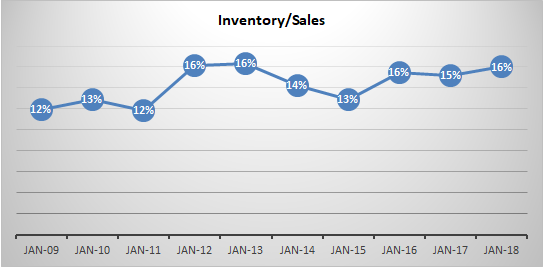

- Working capital intensive operations - Its working capital intensive business with working capital cycle remaining between 100 - 180 days. These will also depend on dispatches during the year end.

- Loans and advances extended to Arvind Ltd, its parent: Anup has extended interest bearing loans & advances of Rs.40 crore as on March 31, 2019 to its parent. However, the same can be called back depending on Anup’s fund requirements as per management.

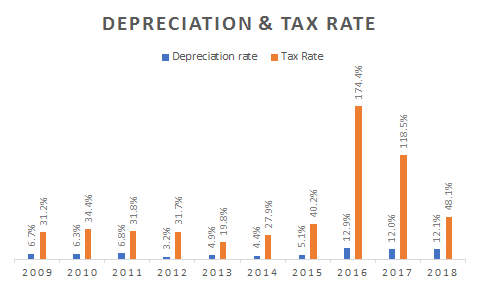

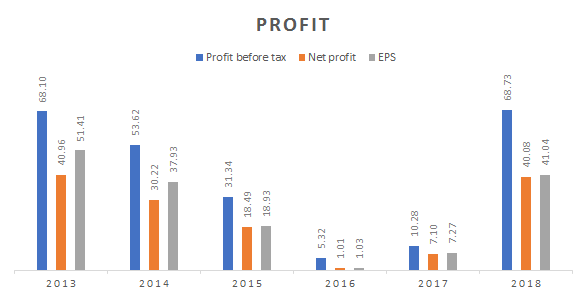

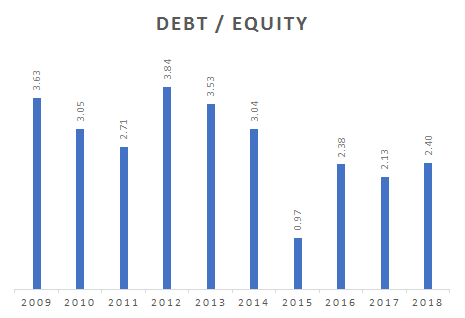

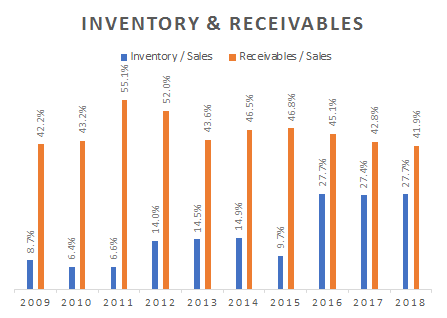

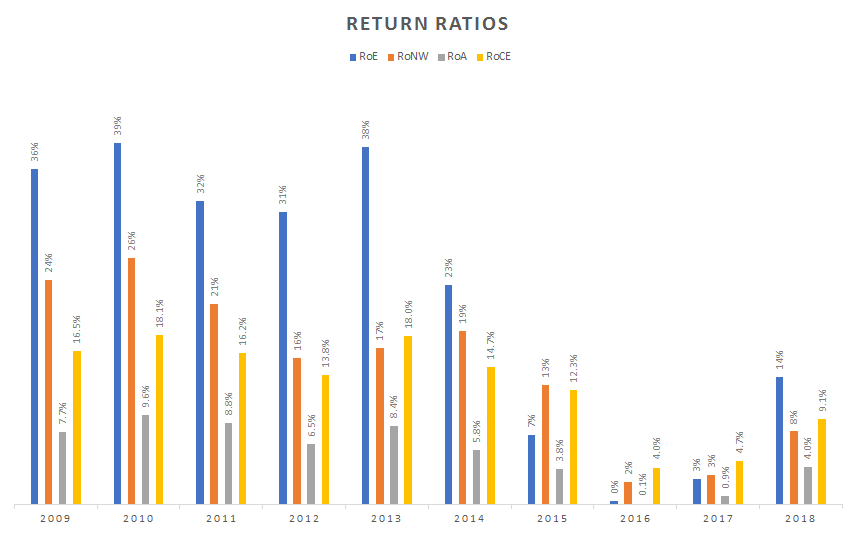

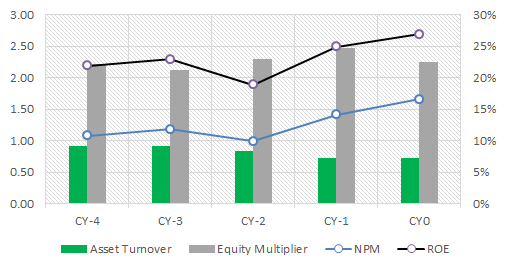

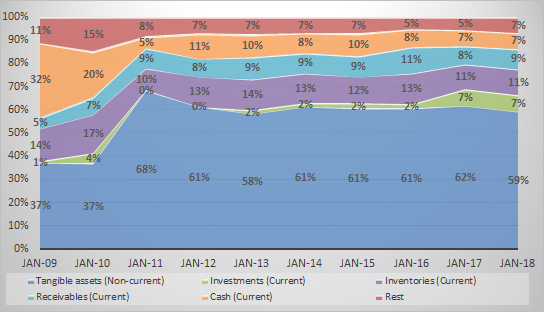

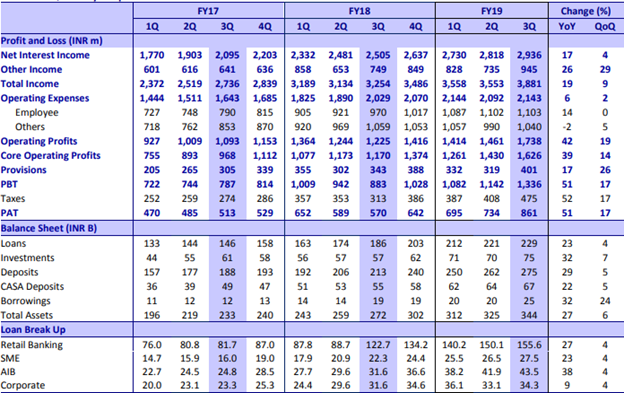

Key Financials:

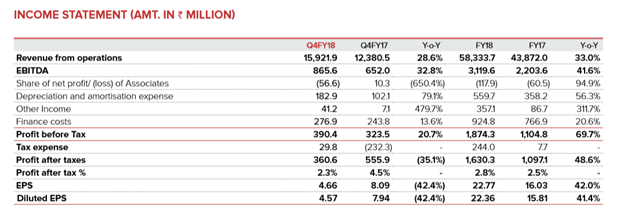

Profit and loss & key ratios

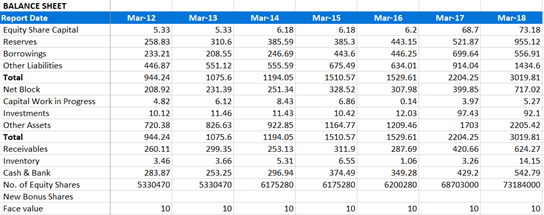

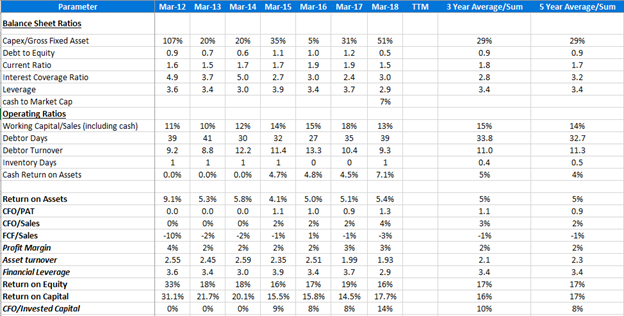

Balance Sheet & Key Ratios

(Disclosure: Invested. This is not a recommendation and anyone contemplating buying or selling should do their own diligence or take advice of their financial advisor)

Q4FY19 Results.pdf (2.8 MB)

Anup Engineering_VP Presentation_2019_For Uploading.pptx (923.0 KB)

Information-Memorandum_The-Anup-Engineering-Limited.pdf (3.0 MB)

Posts: 10

Participants: 5