-

4800+ Rooms across 31 Hotels

-

Owns the properties - Refurbishes, renovates and then lets out the hotel to big hotel brands to manage it

-

Samhi doesn’t manage or operate the hotels itself

-

Passes on the management fees and retains the F&B and rental incomes

-

75% is room rental; 25% from F&B

-

Hotels / Brands:

- Courtyard by Marriott

- Fairfield by Marriott

- Sheraton by Marriott

- Renaissance by Marriott

- IHG

- Hyatt Place

- Hyatt Regency

- Holiday Inn

-

Owned by Samhi and managed by Marriott / IHG / Hyatt (charges mgmt. fees to Samhi)

-

90% of their revenues come from Tier-1 cities

-

Hotel traffic tends to be higher in these cities

-

ARRs are higher in these cities

-

Good geographical diversification protecting it from unforeseen situations in a certain city / region

-

Focuses a lot on office space absorption, which is on the rise (lot of scope in cities like Bangalore, Mumbai, etc.)

-

Commercial activity has picked up and expected to stay robust going forward

-

Air passenger traffic remains strong, showing good travel demand

-

Demand is not a problem as per management

-

Creating supply takes time and that provides companies like Samhi with high pricing power – driving up the ARR, Occupancy and therefore, the RevPar

-

Good time to play the upcycle until the supply comes in and demand starts peaking in a few years

-

Three categories of hotels:

- Upper Upscale – ARR – 9300+ (43% of Revenues)

- Upper Midscale – ARR – 5700+ (42% of Revenues)

- Midscale – ARR – 3700+ (15% of Revenues)

![image]()

-

Remains a debt heavy company, but most of the IPO proceeds have been used to pay off the debt (900Cr used for debt reduction) – finance cost has fallen

-

Management expects the growth in profitability to aid in debt reduction going forward

-

RevPAR is on the rise, growing at 20% YoY in the recent quarter

-

EBITDA margins at 32%

-

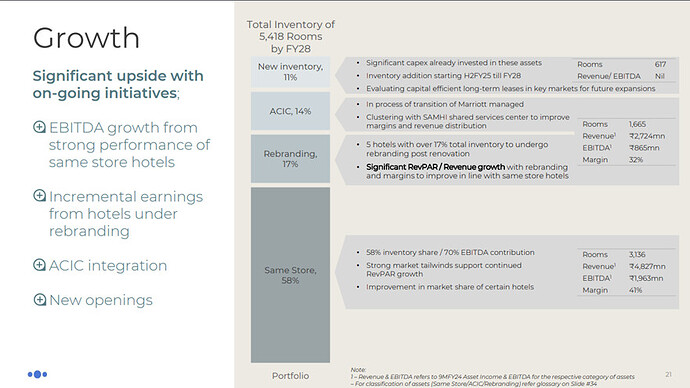

ACIC Hotel Chain acquired. Being managed by Samhi as of now, will be passed on to Marriot to manage by Q1 or Q2 FY25

-

962 rooms in ACIC Portfolio; 22% of the revenues as of now

-

As all these rooms become operational and occupied, EBITDA margins are expected to touch 40%+ (8-10% improvement)

-

Being a primarily business hotel model, occupancy on weekdays is better for Samhi compared to weekends (78-80% on Tue, Wed and Thu; 64-67% for Sat-Sun)

-

Weekend occupancy is also expected to improve in FY25-FY26 as per mgmt.

-

Not acquiring too many new hotels; major focus is on increasing revenues from existing hotels through renovation and refurbishment

-

Made provision for lease cancellation issue of around 7Cr

-

Finance cost has come down from 132Cr to 65Cr; expected to come down further as they deleverage

-

Samhi is pursuing a long term lease arrangement (which will be tied to revenues)

-

Will become a completely asset light model - reducing depreciation and help margins further

-

Expecting strong H2 performance in FY25 with new inventory boosts

-

Looking to turning profitable by Q1FY25

Risks:

- Extremely cyclical sector

- Company has a lot of debt

- Yet to turn profitable

Disc: Invested

85 posts - 43 participants